How to scale a fintech when the market gets tough

By Gisela Crescipulli, Creative Brand Strategist

Strategy, marketing, and innovation.

What really changes when new players like Revolut enter the market?

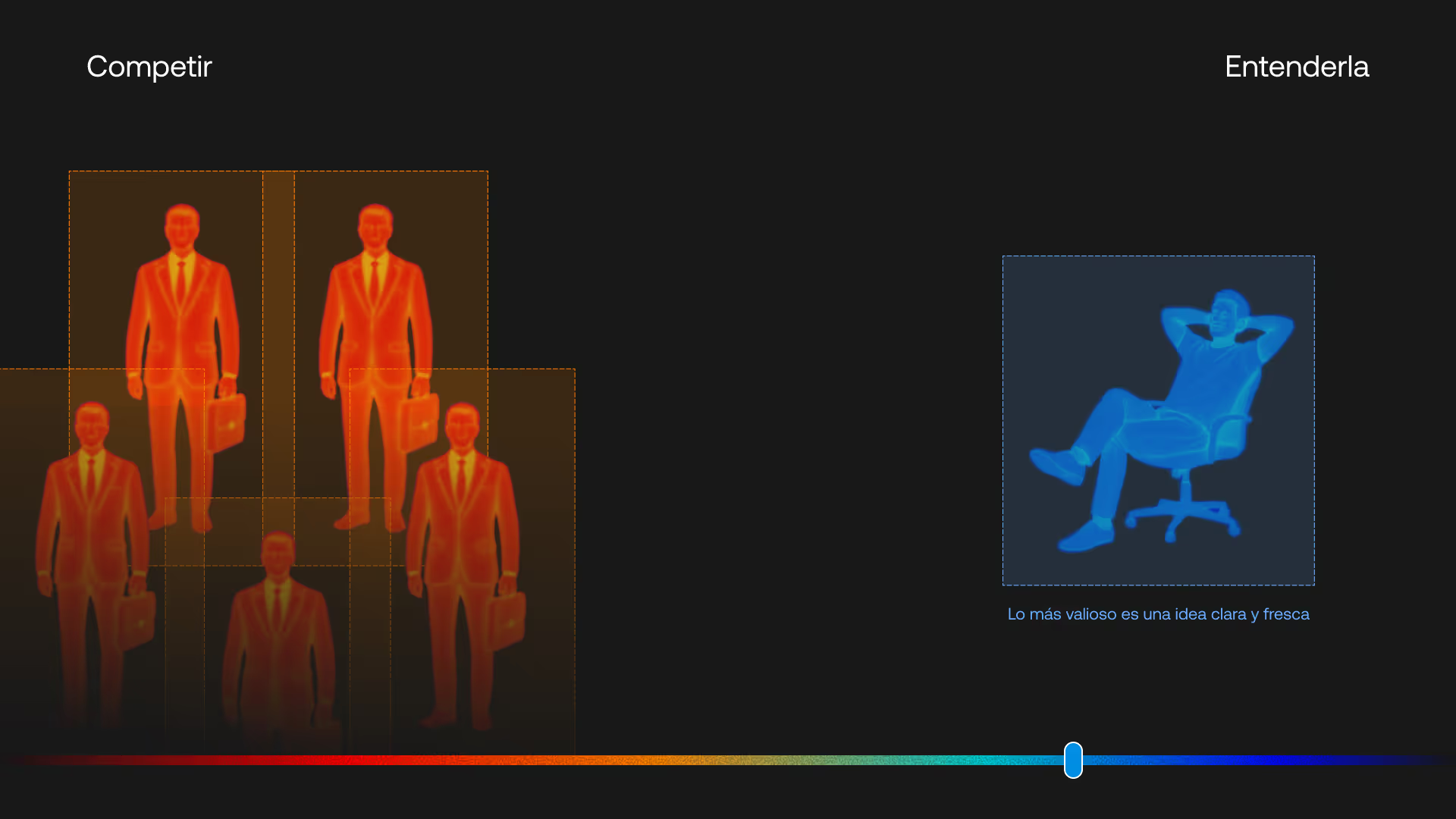

When a market fills up with competitors, the advantage doesn’t come from doing more things or reacting faster. It comes from having a clear central idea, what problem you solve and for whom, and executing it with precision.

That’s what keeps a fintech or a bank relevant when the bar rises: a value proposition that reduces friction, can be understood in seconds, and holds up across the entire experience.

In Argentina, the noise around the arrival of new players (like Revolut opening a waitlist and signaling its intent to launch locally) is more than just news. It’s a sign of the times. The competition is no longer about “more apps,” but about better models.

The new fintech landscape: growth, adoption, and increasingly demanding users

To understand why this moment matters, a few numbers are enough:

- In Argentina, the digital wallets and prepaid cards market is projected to reach USD 9.84 billion by 2025, growing at 16.6% annually.

- Fintech adoption is already around 67%.

- Globally, fintech still represents only about 3% of banking and insurance revenues, but it grows three times faster: in 2024, +21% year-over-year vs. ~6% for the rest of the financial sector.

- In Argentina, the ecosystem reached 383 fintechs in 2024, growing at an annual rate of approximately 15.3% between 2020 and 2024.

Growth brings opportunity, but it also raises expectations.

The real challenge: standing out when everyone promises zero fees and a “seamless experience”

The arrival of global brands raises the baseline: frictionless onboarding, low costs, polished UX, fast support, integrated products.

The common trap at this stage is assuming the answer is to add more features.

In demanding markets, isolated functionality rarely moves the needle. What truly differentiates category leaders is:

- a clear, defensible central idea,

- an end-to-end experience, and

- an operating model that can scale without breaking.

For example, the BNPL market in Argentina is estimated at USD 2.15 billion in payment volume by 2025.

As these categories grow, users quickly get used to better experiences. And once that happens, “promising the same thing” stops working.

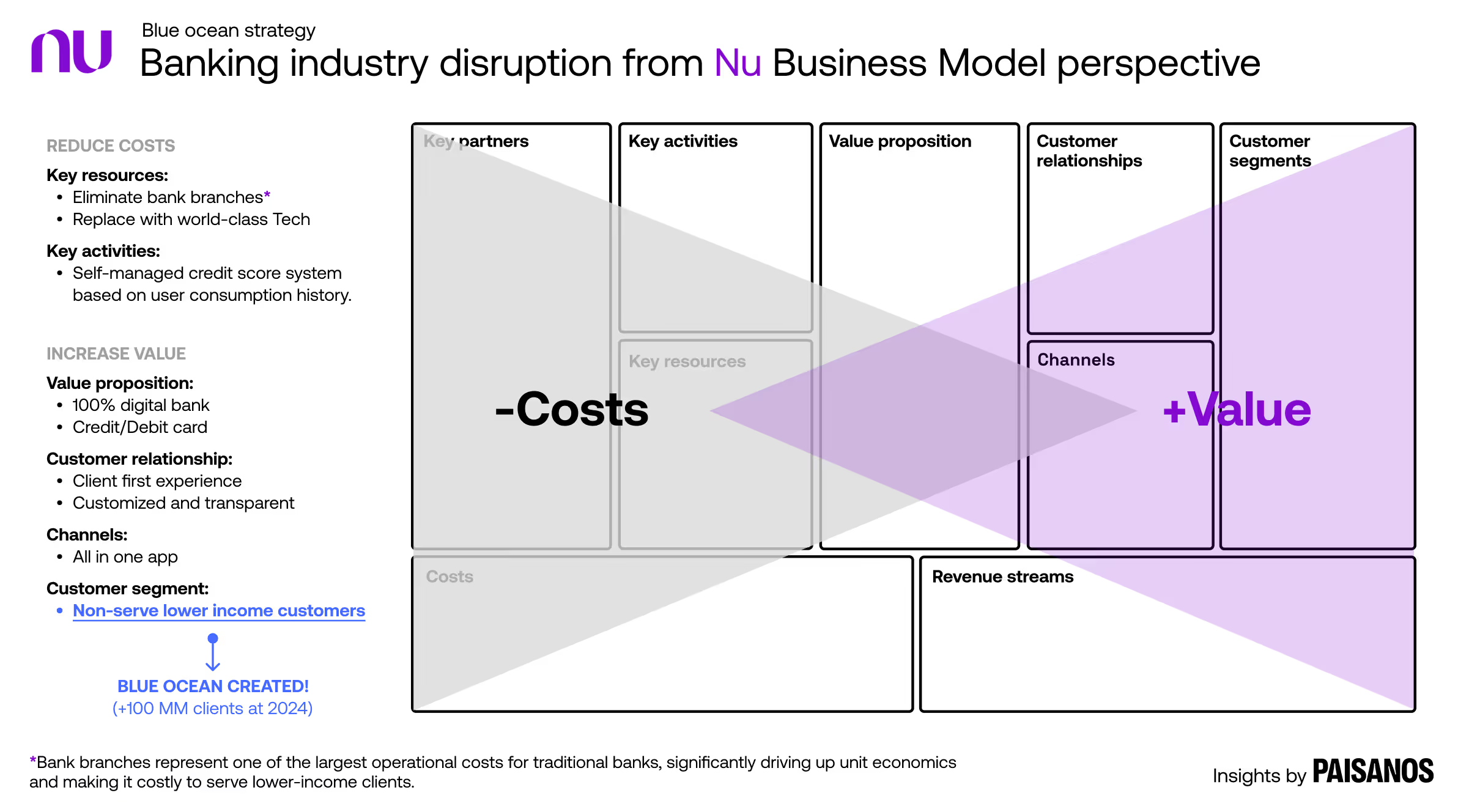

A useful mirror: what Nubank did to change the rules

A concrete example of how this race is won is Nubank. Its growth isn’t explained by “having more products,” but by simplifying the entire system.

The formula (easy to say, hard to execute) was:

- eliminating physical branches,

- automating critical processes (onboarding, risk decisions), and

- building a value proposition centered on transparency and experience.

The result was a lighter model with structurally lower costs and an experience that reshaped user expectations across the region.

The key question this case leaves behind isn’t “Which feature should I add?” but:

What are you going to build that others still can’t offer consistently?

You can dive deeper into their story and model in this full Nubank analysis.

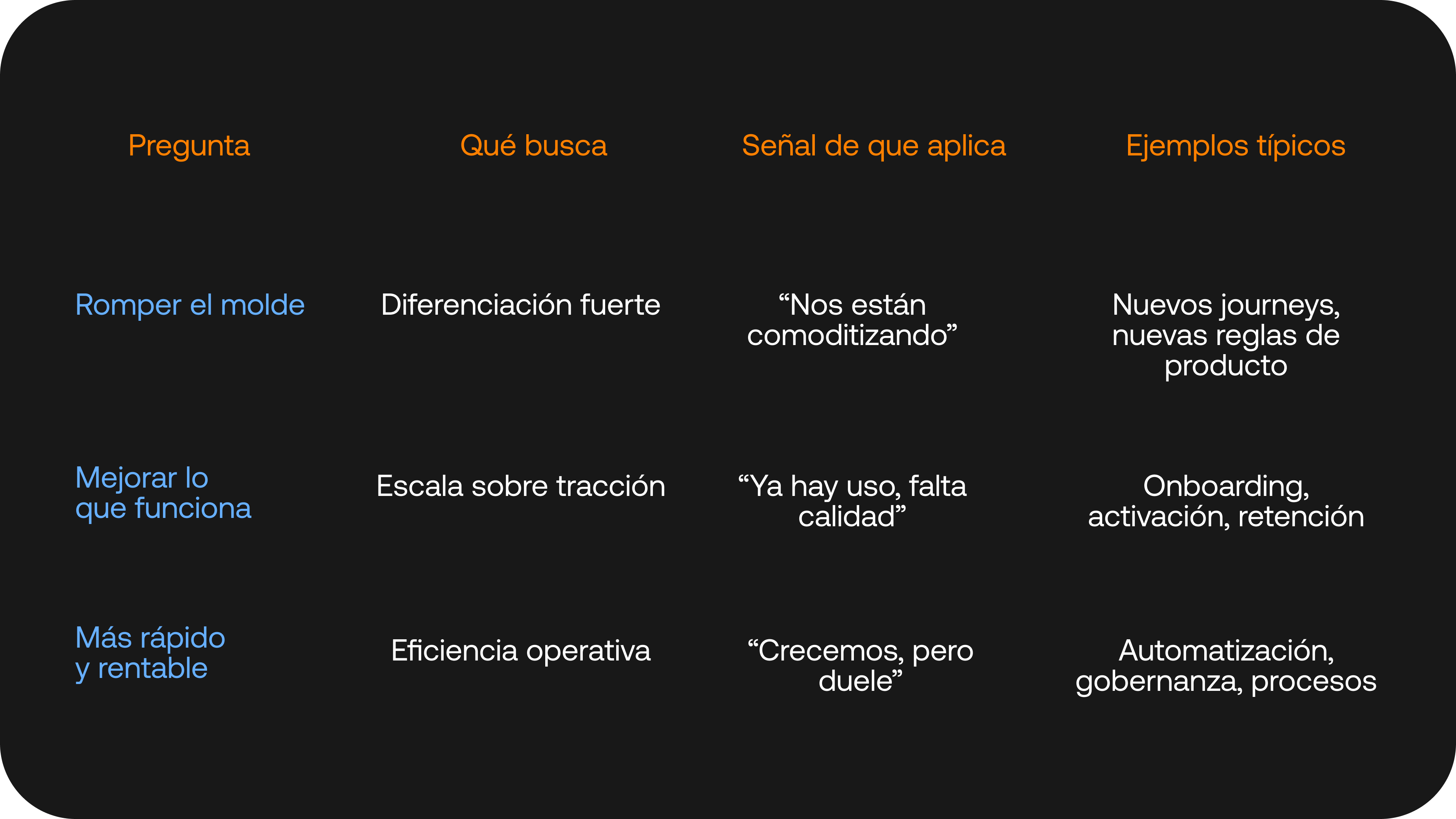

Three questions to innovate with purpose (not anxiety)

When we work with organizations looking to scale, we usually frame the conversation around three questions that help prioritize decisions.

1) How can we break the mold? (Disruptive innovation)

Changing the rules of the category: a new experience, a new model, a new way of capturing value.

2) How can we improve what already works? (Sustaining innovation)

Raising the bar where there’s already traction: better flows, performance, and retention.

3) How can we make it faster and more profitable? (Efficiency-driven innovation)

Reducing costs, automating processes, improving time-to-market, and standardizing without losing quality.

This framework helps avoid innovation driven by hype and instead aligns effort with real business needs.

Real cases: from idea to execution

MODO: speed as a competitive advantage

When MODO came to Paisanos, the challenge was clear: launch in a market dominated by established players.

The strategic focus leaned heavily on the question “How do we break the mold?” — designing an experience so intuitive and natural that it could become a new standard.

Results (based on data from the Paisanos case):

- +10 million downloads

- +100 million transactions

- 4.8/5 average rating

Read the full MODO case here.

Banco Galicia: transformation starts with culture

At Galicia, the challenge wasn’t launching something new, but scaling internal capabilities: improving what already existed and making it more agile.

The work focused on sustaining and efficiency-driven innovation, training teams, designing and testing models, and shifting from an operational mindset to managing a portfolio of initiatives with different risk levels.

Read the full Banco Galicia case here.

How to spot opportunities when competition multiplies

If you want to scale when “everyone promises the same thing,” you need method. These ideas help turn strategy into action:

- Map real frictions: costs, delays, frustrations (onboarding, recurring payments, claims, limits, support).

- Identify underserved segments: audiences that aren’t well served (unbanked users, mid-sized cities, older adults, SMEs with specific needs).

- Design complete experiences: not a feature, but a coherent journey — from acquisition to habit.

- Test fast, learn faster: evidence usually beats waiting for the “perfect version.”

- Scale with governance: initiative portfolios, clear ownership, metrics, and investment proportional to risk.

Two trends that will shape fintech in 2025

Advanced cybersecurity as a standard

As digitalization increases, so does the attack surface. MFA, biometrics, and AI-driven fraud detection are no longer “nice to have.”

Open finance as the default

API-based integration and personalized product orchestration become inevitable. Competitive advantage emerges from how you combine data + product + experience.

Now is the moment to change the rules of your game

Revolut’s arrival doesn’t mark the end of local fintechs. It marks the beginning of a phase where standing out will matter more than ever.

In a more demanding market, a clear idea is the most valuable asset. The real question isn’t whether you’ll transform, but when and with what purpose.

If you’re looking to scale with strategic vision, transform your culture, or design products that reshape a category, we can help.

Explore our other cases or book a conversation to see what we’re thinking.

Frequently asked questions

What changes when a global competitor enters a fintech market?

Experience standards rise: onboarding, support, costs, and usability become comparable. Expectations increase and tolerance for friction drops. The response is rarely adding features, it’s clarifying a defensible value proposition and executing an end-to-end experience.

How does a fintech differentiate when “everyone promises the same thing”?

By defining a central idea (what you solve, for whom, and why you’re better) and translating it into a complete journey: acquisition, onboarding, habit, support, and trust. Features can be copied; coherent, well-operated systems are harder to replicate.

What does it mean to innovate with purpose in fintech?

It means prioritizing initiatives based on the type of change the business needs: breaking the mold (disruptive), improving what works (sustaining), or making it faster and more profitable (efficiency). This avoids innovation driven by trends and helps allocate resources with clear metrics.

Which fintech trends should we follow in 2025?

Two cross-cutting forces stand out: advanced cybersecurity (MFA, biometrics, AI-driven fraud detection) and open finance as the default (API-based integration). Companies that orchestrate data, product, and experience to deliver personalization with trust will build more sustainable advantages.